The Euro (EUR) has been struggling for a few months now. The European Central Bank (ECB) remains one of the most dovish central banks of the major currencies and this continues to dampen the relative performance of EUR. The promise of a forward guidance review at the July meeting has failed to stoke any fires of recovery.

The doves remain in control of the ECB, so the market remains unconvinced that anything will materially change in the July meeting.

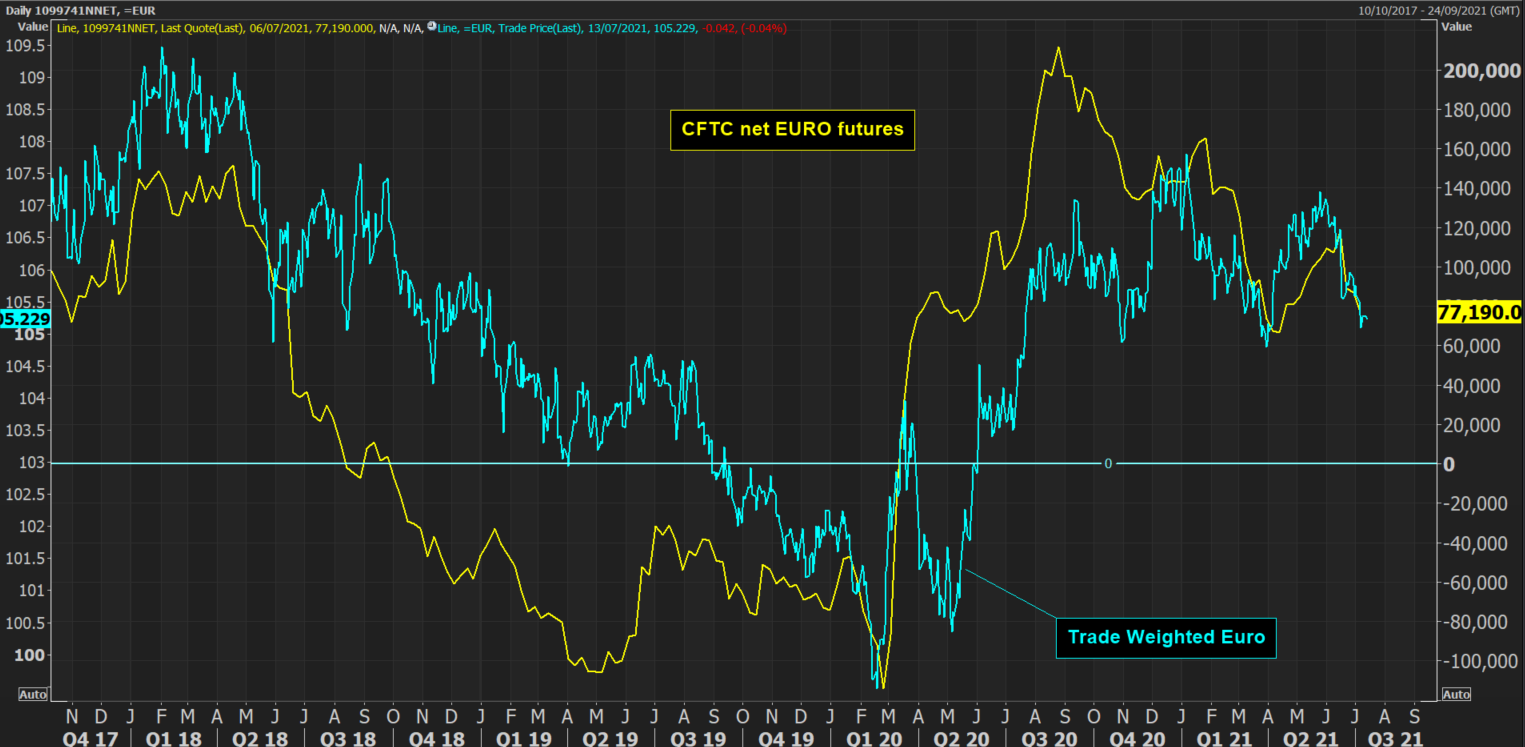

Net Euro futures shows the market is steadily closing out long positions, pulling the trade-weighted Euro lower

With a more resilient USD, this will keep negative pressure on EUR/USD

ECB change in forward guidance at the July meeting

Yesterday’s interview on Bloomberg with ECB President Christine Lagarde suggested that we should be preparing for new guidance on monetary stimulus in the ECB meeting at the end of July. There would be fresh measures to support the Euro-area when the emergency €1.85 trillion PEPP stimulus comes to an end in March 2022.

This comes after completing their Strategy Review which changed the inflation aim from “close to, but below, 2%” to being “2% over the medium term” which would also allow room to overshoot its target. It seems that the ECB remains solid in its position as one of the most dovish of the major central banks.

Eurozone bond yields have barely registered this prospect of allowing higher inflation. If anything they have shifted lower again, whilst US yields have ticked slightly higher. If this continues it will continue the negative pressure on EUR.

EUR futures still net long, with room to close out longs

EUR has a tight correlation with the direction of the CFTC net Euro futures positioning over the medium to longer term. Futures positioning has been closing out a sizeable net long positioning over the past nine months. Over time this is acting as a drag on the trade-weighted Euro.

If the dovish outlook from the ECB continues, then more of the net longs on EUR futures will be closed. This will further drag the trade-weighted Euro lower.

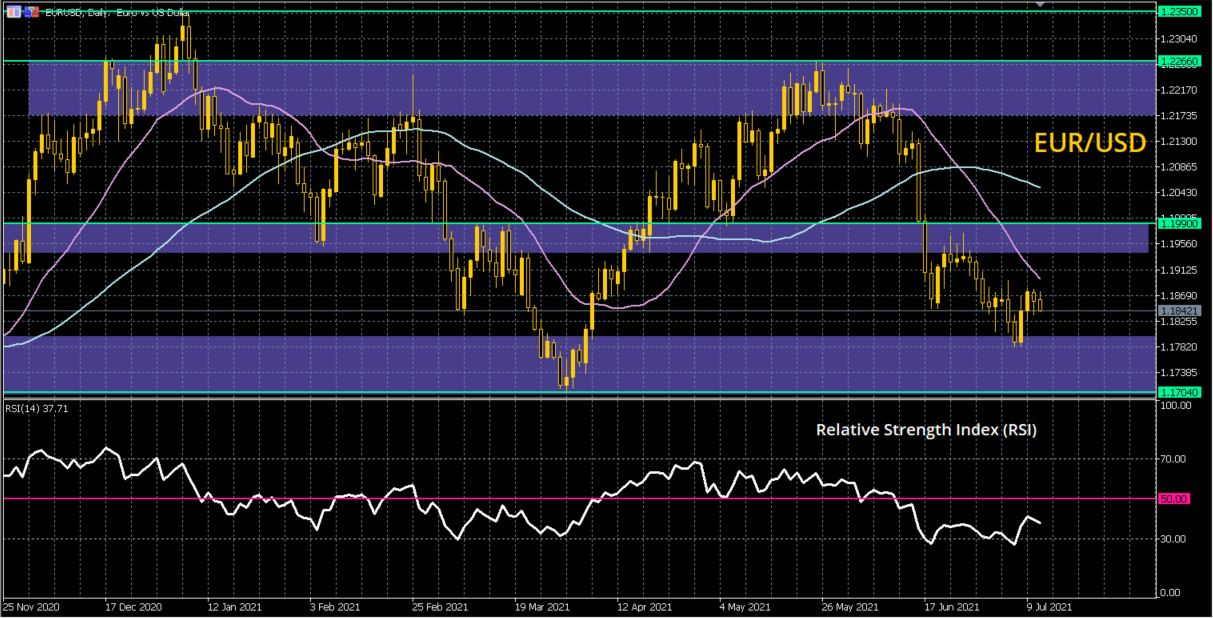

EUR/USD increasingly looks to be a sell into strength

With the Federal Reserve shifting its stance on the potential for the first rate hike into 2023 (and possibly sooner) this is driving more underlying support for USD. Coming where the ECB is so dovish (which is putting downside pressure on EUR) means that EUR/USD has a negative bias.

Looking at the technicals, we have seen a run of lower highs and lower lows since late May. The key downside shift was in mid-June when the Fed signalled its hawkish surprise on rates. This move now leaves 1.1950/1.1990 as a key medium-term resistance band on EUR/USD.

One interesting technical analysis indicator to keep an eye on though is the MACD, as it has just crossed higher to give a near to medium term buy signal. This may pull a technical rally. The key resistance to watch would be 1.1895 and a close above would pull the market into 1.1950/1.1995 which we now see as a prime sell-zone.

This MACD buy signal is just one signal and for now, it is just a warning sign of a possible rebound. Ultimately, we see a sustainable EUR recovery against USD as unlikely. We therefore now see rallies as a chance to sell on EUR/USD. We are looking for downside pressure towards the key support area 1.1700/1.1780.

Conclusion

The dovish leanings of the ECB will keep the EUR from any sustainable recovery. With the US dollar beginning to find more support, we believe that this means EUR/USD will trade with a negative bias.