What we are looking at today:

- USD regaining strength: The USD has rebounded overnight following a hawkish lean in a speech by Fed Chair Powell. This now becomes an important moment for major markets that had been looking to recover in recent days.

- Indices are holding their recovery, for now: European indices have recovered well, but the rebound is stalling this morning. Will be once more be a chance to sell?

- Crypto rebound rolling over: If indices fall back then so will cryptocurrencies such as Bitcoin.

- Data trading: Eurozone final inflation is unlikely to cause much of a stir, whilst only a significant surprise in the US housing data will do much to the USD. Canadian inflation could be where the action is, especially for CAD traders.

Overview

Market sentiment has been recovering well since the end of last week. Markets moved on a dovish hint from Fed Chair Powell on Thursday. However, in his latest speech last night, there were little other than hawkish hints. Markets are once more reacting. US yields have moved higher again and the USD has looked to regain some of the lost ground of recent days. US equity futures are pointing to a lower open today.

This now becomes a key moment for markets. Previously, risk rallies on the likes of the Aussie, Sterling, and equity indices have been seen as a chance to sell. If these rallies simply wilt once more and start breaking the supports formed in recent days, then selling pressure could take off once more.

The economic calendar is packed with tier one data today. Final Eurozone inflation is not expected to see any revisions, so may see a muted market impact. US Building Permits and Housing Starts are also fairly minor US housing data but are always worth watching for surprises. The Canadian inflation will certainly be interesting for CAD traders. Will it match US inflation with an upside surprise?

Today's news

Market sentiment is starting to weaken again: A hawkish lean from Fed Chair Powell has nipped a risk recovery in the bud. USD is strengthening again, with US futures showing a rolling over on Wall Street this morning. Once more a risk deterioration is pulling cryptocurrencies lower.

Treasury yields have increased: After a few days of consolidation, Treasury yields moved higher yesterday in the wake of Fed Chair Powell’s speech (see below). The move has been held today.

Fed chair Powell leans hawkish: After markets reacted on Friday to a surprise dovish reference to a speech by the Fed Chair, there has been another reaction overnight. Powell’s speech yesterday was leaning back towards hawkish this time, discussing the focus on getting inflation down. He confirmed the broad support on the FOMC for two 50bps hikes in the June and July meetings. He also intends to get the rate back towards neutral by Q4, although they are not sure what neutral is (potentially c. 2.5%). However, they could go above neutral (moving to tight monetary conditions) to get inflation down.

Japanese GDP declines less than expected in Q1: QoQ GDP fell by -0.2% in Q1 (after growth of +0.9% in Q4). This was slightly better than the -0.4% consensus forecast.

AUD hit as Australian wage pressures ease: Rising wages have been a key factor in the more hawkish rhetoric from the Reserve Bank of Australia. However, wages increased less than expected in Q1, with YoY wage growth at +2.4% (up from 2.3% in Q4 but missing the 2.5% expected). This is weighing on AUD this morning.

UK inflation in line with expectations: Headline UK CPI has increased to 9.0% in April (from 7.0% in March). The sharp increase was expected and came in line with forecasts. Core CPI increased to 6.2% (from 5.7%) and was also in line.

Cryptocurrency faltering as risk appetite deteriorates again: Once more we are seeing a strong positive correlation between cryptocurrencies with risk appetite (and specifically the NASDAQ). NASDAQ futures are lower, and cryptos are falling back again. Bitcoin is c. -1.0% this morning and back below $30,000 once more.

One Fed speaker: the FOMC’s Patrick Harker is the only Fed speaker today. Harker is a voter in 2022 and 2023 and is broadly hawkish. His speech is at 2100BST.

Economic Data:

- Eurozone inflation - final (at 1000BST). Consensus is not expecting any revisions today to the headline HICP at 7.5% and core HICP at 3.5% in April.

- US Building Permits (at 1330BST). Consensus is expecting a slight decline to 1.812m in April (down from 1.870m in March)

- US Housing Starts (at 1330BST). Consensus is expecting a slight decline to 1.765m in April (down from 1.793m in March)

- Canada CPI (at 1415BST). Headline inflation is expected to remain at 6.7% in April (6.7% in March) whilst core inflation is expected to decline slightly to 5.4% (from 5.5%)

Major markets outlook

Broad outlook: Sentiment has started to deteriorate once more. Leading to the USD performing well again which is impacting major forex and commodities. Indices are stalling.

Forex: JPY is performing strongly, along with the USD. GBP, EUR, and AUD are underperforming.

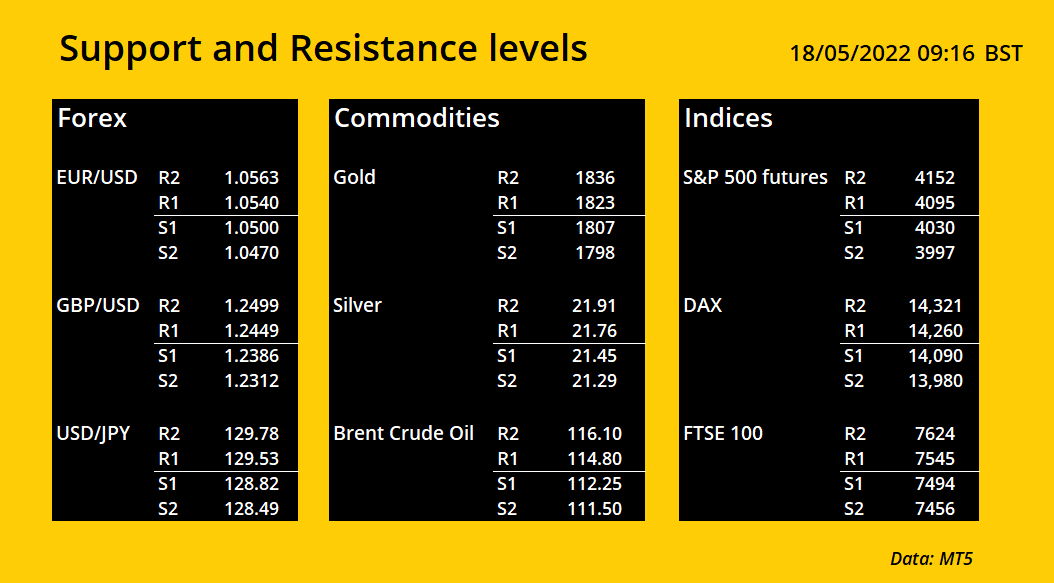

- EUR/USD saw a strong recovery through the overhead supply at 1.0470/1.0500 from a raft of late April/early May lows. This has improved the outlook, but as the market has rolled over this morning, the 1.0470/1.0500 area now becomes an important gauge of near-term support. Lose this as the outlook turns sour again with a likely retest of 1.0350. Initial resistance at 1.0563 is now a barrier to the 1.0600/1.0640 key resistance.

- GBP/USD remains volatile as a swing higher in recent sessions has started to retrace this morning. Reaction around 1.2400 will be an important gauge for the recovery. This is a near-term pivot area and decisively losing this support will re-open the downside towards a test of 1.2295 and potentially back to the key low at 1.2155. Initial resistance at 1.2500 is now a barrier to the next key resistance at 1.2635.

- AUD/USD has been consolidating around the old overhead supply between 0.6965/0.7030. The market is trading slightly lower this morning, but if there is a close back under 0.6965 it would be a rejection of a rally once more and the market would likely come under renewed selling pressure. However, if this pivot band can hold, and the market move to close above 0.7055 it would be a strong signal of intent to recover now.

Commodities: Precious metals are looking shakey in recovery. Oil is stalling around the top of the seven-week range.

- Gold has eased back to take some of the recovery potentials out of the market that came following Monday’s strong positive candlestick from $1787. The concern for the bulls is that resistance has formed around the old medium-term pivot at $1830/$1850. With momentum still correctively configured, there needs to be a strong reaction today otherwise the negative bias will kick in again. An early pick-up from $1807 ideally now needs to hold as initial support.

- Silver has lost some of its recovery momenta as the resistance of the overhead supply between $21.40/$22.00 has proved to be a barrier to gains. Despite this though, there is still support around $21.30/$21.40 holding this morning. . This seems to be a bit of a crossroads moment for Silver.

- Brent Crude oil has rallied to test the resistance of the seven-week trading range between $99/$116. Yesterday’s initial test has just eased back, but the market is trading higher this morning and is in a position for another go today. Momentum is still tentative with the RSI hovering above 50. A close above $116.10 would open upside towards the next resistance around $124. Initial support is at $111.50 and then $109.50.

Indices: A decent recovery in recent days is looking more tentative now. Reaction in the coming days will be key for the near to medium-term outlook.

- S&P 500 futures posted another strong session yesterday to push into the considerable overhead supply area between 4060/4140. However, once more this is just beginning to ease back slightly. Reaction to this overhead support could be key to the near to medium-term outlook now. A close above 4140 would be a strong signal of intent to sustain the recovery. A bull failure below 4040 would be disappointing but below 4380 would renew the downside momentum.

- German DAX has broken some important resistance in recent sessions. The four-and-a-half-month downtrend has been breached and is also trading decisively above the 55-day moving average (c. 14,027) for the first time since early January. Previous rallies have faltered with the RSI around 50 but momentum looks to be improving now. The crucial question is whether a near-term decline is bought into. The support around 14,090 will be watched, but below 13,855 re-engages selling momentum. If the market could push above 14,321 (the first key lower high) it would be a positive signal for sustaining recovery.

- FTSE 100 has rallied well in recent sessions but is starting to lose some of the momenta in the move. Reaction to initial support around 7475/7495 will be key now as losing this will once more see this as a selling opportunity rally. Initial resistance is at 7545 which is a barrier to 7625.

This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. INFINOX is not authorised to provide investment advice. No opinion given in the material constitutes a recommendation by INFINOX or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.