What are we looking at

- The oil price is advancing once more and this is pulling bond yields higher. However, the USD is mixed as commodities gain ground leaving CAD and AUD performing well.

- Indices moving higher: Indices are being helped by the higher oil price, for now. Major oil producers are making strong gains but this comes with a caveat. Can indices continue to move higher as the inflationary implications of higher oil prices begin to weigh again?

- More ECB speeches: The ECB’s Forum on Central Banking continues today. This will be watched for more views on how aggressive ECB monetary policy will be. EUR traders will be alert.

- Data trading: There is a bulk of US data, with Consumer Confidence the big one at 1500BST. There are also other lower-tier announcements, with the US Goods Trade Balance at 1330BST, the Case-Shiller house prices at 1400BST and the Richmond Fed at 1500BST.

Overview

As the European session has taken hold on Tuesday there has been an increasingly strong look to the oil price. Supply restrictions on oil (with Saudi Arabia and the UAE seemingly unable to increase production much further) are fuelling the gains in oil. This is driving gains on major oil equities, helping indices higher. Furthermore, in forex, the commodity currencies (AUD and CAD) are outperforming. However, this is also pulling US bond yields higher once more on the inflationary fears of higher oil prices, pulling USD/JPY higher as a result.

The question is whether the gains on risk-positive assets that are coming today can continue if inflationary fears from higher oil prices worsen? This does not tend to be a combination that is the bedrock for stable recoveries on indices. The gains seen early in yesterday's European session ebbed away into the US close. Will we see similar moves gain today? It is interesting to see the DAX underperforming FTSE 100, this tends to be a sign that risk appetite is tentative in recovery.

There is a US focus once more on the economic calendar. The deficit in the US Goods Trade Balance is expected to deteriorate once more, whilst US house prices are expected to continue to grow at an annual rate of over 20%. Consumer Confidence is expected to drop again towards 100 which would be 16-month lows. After the Dallas Fed manufacturing data deteriorated and missed estimates yesterday, the focus will be on whether the Richmond Fed can buck the trend today

Today's news

Market sentiment looks more positive, for now: Higher oil prices are helping indices higher for now. Furthermore, risk-positive currencies such as CAD and AUD are outperforming. Silver is outperforming gold in posting gains.

Treasury yields tick higher again: Yields are higher in a slight “bear steepener” (US 10yr yield +3bps, US 2yr yield +1bp).

Saudi and UAE oil production limits: According to reports, French President Macron has spoken with the crown prince of the UAE who said that the UAE is producing near capacity and Saudi Arabia could only increase production by small amounts more. It has been hoped that the big OPEC members would be able to make up for the shortfall of Russian production that has come with the sanctions. The Brent Crude oil price is around +1.5% higher this morning after gaining +1.7% yesterday.

UK MPs voted to support the Northern Ireland Protocol bill: The UK Government is introducing a bill that would look to over-ride the treaty signed with the EU. This is an ongoing situation that could be a drag on GBP performance.

Cryptocurrencies remain under pressure: Crypto fell into the close on Wall Street last night and has failed to make any gains from higher indices this morning. Bitcoin is -0.2% and is back under $21,000

Economic Data:

- US Goods Trade Balance (1330BST) The deficit is expected to widen to -$122bn in May (from -$106bn in April).

- Case-Shiller HPI (1400BST) Houe prices growth is expected to be +21% in April (from 21.2% in March).

- CB Consumer Confidence (1500BST) Confidence is expected to drop to 100.4 in June (from 106.4 in May).

- Richmond Fed Manufacturing (1500BST) The survey is expected to drop to -12 in June (from -9 in May.

Major markets outlook

Broad outlook: Sentiment has tried to improve but looks tentative this morning.

Forex: CAD and AUD are strong, whilst JPY and NZD are underperformers.

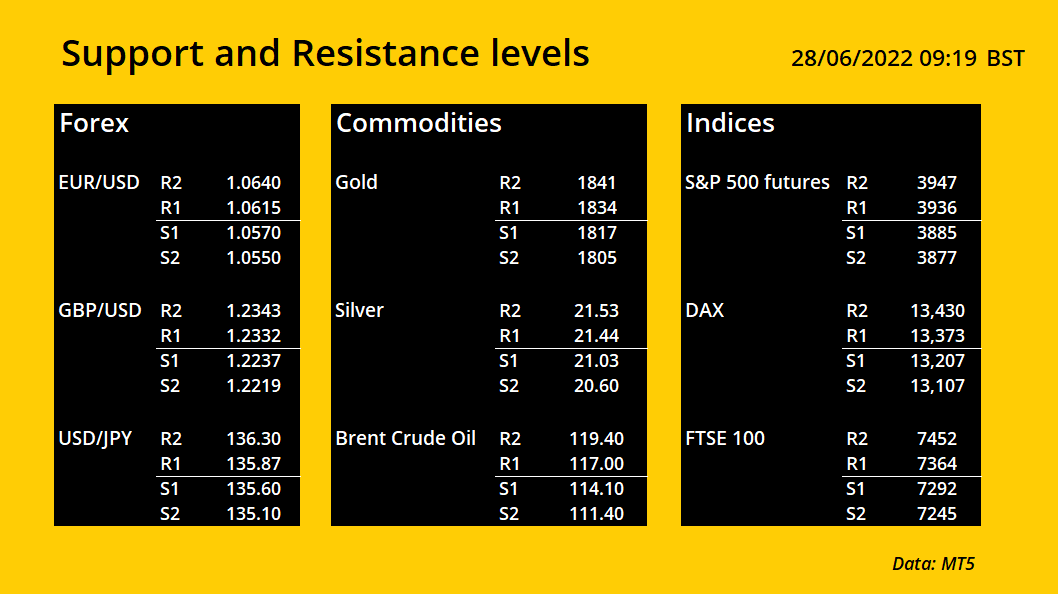

- EUR/USD has ticked a shade higher as the European traders have taken control today. However, the market is still just creeping higher towards a test of the resistance around 1.0600/1.0640 which has acted as a pivot within the range. The key 10-week downtrend also comes in around 1.0650 as resistance. This is coming to another important inflexion point. We still prefer to use near-term rallies as a chance to sell for moves back towards the 1.0350 support area. 1.0470 is higher low support.

- GBP/USD has been stuck for over a week now under the 1.2330/1.2410 resistance area as the market has consolidated above support at 1.2160. Very small candlestick bodies in each of the past 5 completed days reflect uncertainty and indecision. However, we still see any attempted rallies within the big 4-month downtrend (today at 1.2470) will likely falter in an ongoing negative bias. Near-term support is at 1.2235.

- AUD/USD has built from the support band 0.6830/0.6870 and is looking to test the trend of lower highs over the past 3-weeks. Above 0.7000 is needed to improve. There is a less negative look to the 4-hour RSI now but a recovery is still yet to be seen.

Commodities: Precious metals and oil have rebounded in the past couple of sessions, but retain near-term negative trends.

- Gold has sustained its negative bias with another disappointing decline into the close last night. A tick higher this morning is holding up the selling pressure but the outlook remains broadly negative within the 4-month downtrend. Essentially the past 6-weeks have been a trading range, but there is a negative bias that continues to weigh on the price. Initial resistance is at $1841/$1848 but a move above $1857 would be needed to start an improvement in outlook. However, the RSI momentum continues to falter around 50, so we still favour selling into strength.

- Silver fell over at $21.53 to continue a run of lower highs which is building a shallow 3-week downtrend within a 6-week trading range ($20.45/$22.50). However, the RSI continues to falter around 50 which leaves a slight negative bias to the range and leaves a preference to sell into strength for moves to retest the $20.45/$20.60 range lows. Resistance at $21.95 is growing in importance.

- Brent Crude oil has moved higher in the early part of this week and is now looking to break back above the mid-range pivot area of $112/$116. The configuration of momentum on the RSI suggests that the outlook is all but neutral as the market has rebounded in recent days towards the pivot again. However, a close above $117 resistance would improve the outlook once more. Support at $107.65 prevents a move towards $98/$102.

Indices: Indices are building from support this morning, but can this continue?

- S&P 500 futures fell back into the close last night but have picked up this morning, using the old gap at 3876/3895 as a basis of near-term support. As the market has rebounded this morning a test of 3948 (yesterday’s high) could be seen but the next real resistance is not until 4065/4100. Reaction to 3876 support and 3948 resistance will be indicative of the next move. The RSI will be watched as an unwind has come back to 50, whilst the previous rebound faltered around 55.

- German DAX dropped back into the close last night but the bulls are fighting back this morning. There needs to be a move above 13,430 (the first lower high of the recent sell-off) to signal a sustainable shift in the near-term outlook. Alternatively, a faltering of this rally around here would pile the selling pressure back on for what would likely be a retest of the 12,822 low of last week.

- FTSE 100 has been helped by the higher oil price this morning and is strongly higher. The move above 7333 (the first lower high of the sell-off) is also notable but needs to be held into the close. Momentum is improving now with the RSI above 50. The bulls will now look to use intraday weakness into 7292/7333 as a chance to buy. Below 7215 would be a renewed disappointment.

This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. INFINOX is not authorised to provide investment advice. No opinion given in the material constitutes a recommendation by INFINOX or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.