What are we looking at today:

- USD remains strong: The huge run higher on USD/JPY shows no sign of stopping. However, with momentum so overstretched the risk of an unwinding bout of profit-taking grows.

- Indices are threatening lower again: After a choppy period in recent sessions, there are hints of growing corrective pressure once more.

- Data trading: The only data of note comes with US Building Permits and Housing Starts. The market reaction tends to be fairly limited to these but any significant surprises would be worth watching.

Overview

There is a mixed feel around major markets on Tuesday morning after the long Easter weekend that impacted trading volumes across several countries. However, there is a continuation of recent themes that are guiding sentiment. The hawks continue to push their agenda at the Federal Reserve and this is driving higher Treasury yields and hampering any attempts of a bull recovery across equity markets. The renewing military activity in Ukraine is also ramping up tensions once more, this time focused on the eastern regions around the Donbas.

Subsequently, we see the USD broadly consolidating but remaining strong, although the dramatic sell-off on the Japanese yen continues. The Australian dollar is outperforming in the wake of a hawkish lean from the minutes of the Reserve Bank of Australia meeting. Commodities are consolidating whilst European indices have come back from their Easter breaks in a cautious mood and are trading lower. This comes despite US futures holding ground.

The economic calendar only really has a bit of US housing data to concern traders today. Building Permits and Housing Starts are expected to both reduce slightly by around -2% in March. Housing data tends to be at the less important end of the spectrum for market reaction, but it is still worth keeping an eye out for it later today, especially on any significant surprises.

Today's news

Market sentiment remains cautious: With higher yields and a stronger USD, there is a caution that still hangs over market sentiment. European indices have dropped back in early moves as the Russian invasion effort is stepped up again.

Treasury yields continue to rise: Hawkish comments from Fed’s Bullard have once more seen yields pushing higher.

Russian forces advance on eastern Ukraine: The next offensive by Russia in the Donbas has begun. Although this has been anticipated, it is still something that will brace markets.

The RBA meeting minutes: Inflation has picked up and a further increase is expected, with underlying inflation expected to be >3% in Q1 2022. With wages also higher, this has brought forward the timing of the first rate increase.

FOMC’s Bullard hints at being even more hawkish: Bullard (voter in 2022) is the most hawkish of the FOMC members. He has refused to rule out a +75bps hike in the meeting at the end of April, even though it is not his base case (which is +50bps). He is looking for the Fed Funds rate at +3.50% in 2022.

Cryptocurrency holding ground: There has been a sense of consolidation set in over the long weekend. Bitcoin is holding just above $40,000.

Economic Data:

- US Building Permits (at 1330BST). Consensus is looking for a decline of around -2.5% to 1.820m in March (from 1.865m in February)

- US Housing Starts (at 1330BST). Consensus is expecting a slight drop of c. -2% to 1.738m in March (down from 1.769m in February)

Major markets outlook

Broad outlook: Market sentiment is cautious, driven by lower European indices.

Forex: The USD is mixed across majors. JPY is again a big underperformer, whilst AUD is positive after the RBA minutes.

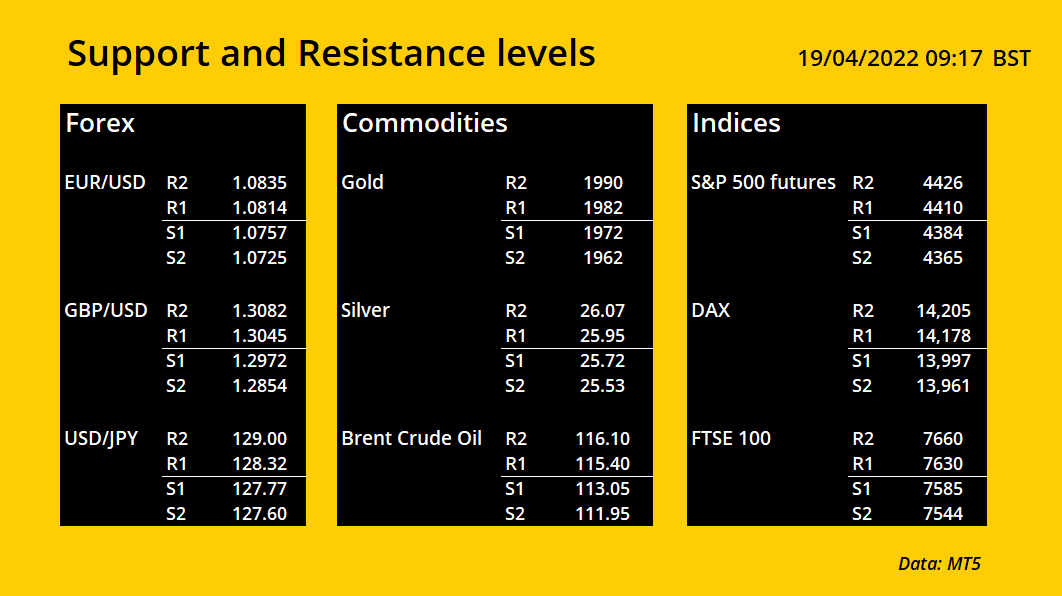

- EUR/USD has fallen away over the Easter break and closed below the old support at 1.0805 yesterday (but on light, holiday volumes). So how the market responds today will be important for confirmation. There is a sense of consolidation this morning but nothing that would hint at sustainable buying pressure. We still look to use intraday strength as a chance to sell. Below 1.0757 opens 1.06/1.07 area.

- GBP/USD has still not closed below 1.3000 despite numerous tests and intraday breaches over recent weeks. A close below 1.3000 would be a signal to suggest further downside. Initial support is at 1.2972 but a move towards 1.2850 would be open. The initial resistance is 1.3045/1.3075.

- AUD/USD has retreated towards the 10-week uptrend (c. 0.7320) which is now an important gauge for the broader recovery. A decent rebound from 0.7340 this morning is a positive response, but there is initial resistance at 0.7390/0.7400 to overcome.

Commodities: Precious metals have fluctuated in recent sessions but continue to trend higher over the past couple of weeks. The oil rally is just showing signs of faltering again in recent sessions.

- Gold remains strong in the wake of a breakout above $1966. Moves have been slightly more choppy and uncertain in recent sessions but momentum remains strongly configured for further gains for a further recovery towards $2000. Intraday weakness continues to be bought into with initial support is now between $1960/$1972.

- Silver has broken through the top of the resistance band at $25.60/$25.85 in a move that opens the key high at $26.95. Although moves have been more choppy of late, with strengthening momentum (RSI now decisively above 60) we look for a move to retest yesterday’s high at $26.21. Intraday weakness is a chance to buy, with initial support around $25.30/$25.60.

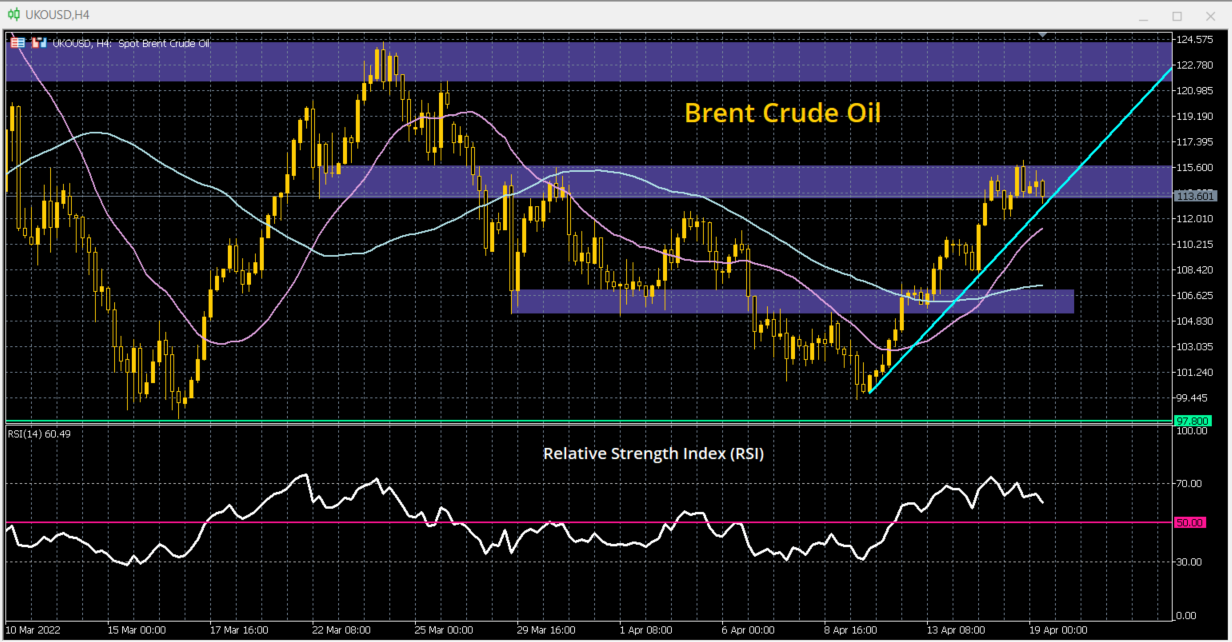

- Brent Crude oil has rallied strongly in the past week and has seen a push above the key resistance at $112.50 which has engaged the next resistance at $115.60. However, the market has dropped back this morning and is looking a little tentative for the first time since the buying pressure was renewed last week. A move below $111.95 would be a near term corrective signal. Resistance is now at $116.10.

Indices: Markets are consolidating but this is within continued corrective outlooks, especially on Wall Street. FTSE 100 continues to hold up well.

- S&P 500 futures have continued to trend lower over the past three weeks and despite a positive session yesterday there is still a corrective outlook that suggests selling into strength. A move above 4466 would be needed to change this outlook. Given the trending move and negative momentum configuration on daily and 4-hour charts, we prefer a retest of 4355 initially and subsequent further downside.

- DAX bulls have stemmed the tide of selling pressure but this may only be short-lived. Although the mini two-week downtrend has been broken, there remains a bigger three and a half month downtrend. This is in addition to falling moving averages and corrective configuration on daily and 4-hour chart momentum. We favour selling into strength. Initial resistance is at 14,205 under the bigger 14,325 resistance area. Initial support is at 13,960 before the recent low at 13,885.

- FTSE 100 has picked up in recent sessions and buyers are still happy to support near term weakness. However, an important moment is now approaching. Another lower high under 7677 would begin to question how much further the market can go in this period. Support at 7526 is growing in importance.

This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. INFINOX is not authorised to provide investment advice. No opinion given in the material constitutes a recommendation by INFINOX or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.