What we are looking at today:

- USD strength quickly resumes: The Fed-driven USD correction lasted less than 24 hours, as USD strength quickly resumed yesterday to claw back all previous losses. This move of strength is continuing today.

- US yields higher again: Longer-dated US yields jumped higher yesterday on fears of what Fed tightening does for US growth. Yields will again be in focus today with Nonfarm Payrolls.

- Indices under selling pressure again: Fears of the negative impact of higher interest rates hitting growth had a decisive selling impact on Wall Street (specifically the big tech stocks) yesterday. Will this continue today?

- Data trading: All eyes will be on the US jobs report, with headline payrolls expected to fall slightly but remain strong at 391,000. Wage growth will also be watched after it jumped to near two-year highs last month.

Overview

There has been enormous volatility in recent days. Key risk events such as the FOMC and Bank of England have swung major markets. Renewed dominance of USD outperformance has taken hold. This has played out through major forex pairs and dragged precious metals sharply lower. The impact of sharply higher US interest rates has also resonated through Wall Street and the big tech stocks specifically yesterday. High rates hit high growth stocks and NASDAQ is under mounting selling pressure.

We see these moves continuing this morning, with the USD again strengthening across major forex. This comes even with Nonfarm Payrolls on the agenda today. Traditional cautious trading ahead of the US jobs report has given way to further risk negative trading. European indices are playing catch up on Wall Street selling, whilst US futures are lower again.

Nonfarm Payrolls loom large on the economic calendar today. Consensus is looking for a slight reduction in monthly jobs growth to 391,000. However, after the ADP employment change missed estimates by around 130,000 jobs on Wednesday, there will be a little caution coming into today’s BLS jobs report. Average Hourly Earnings jumped to a near two year high last month, but the consensus is looking for wage growth to moderate slightly. This is despite the continued tightening of the labor market, with a reduction in unemployment expected too.

Today's news

Market sentiment turns sharply negative again: It is risk negative across the board, with USD outperformance, Indices lower and silver underperforming gold.

Treasury yields higher: Longer-dated yields (the 10 year moving above 3.0%) spiked higher on growth fears yesterday. This is risk negative and is supporting the USD. Yields have a degree of consolidation early today, but are still upwardly biased.

Massive big-tech sell-off on Wall Street: NASDAQ had its worst day since June 2020. Fears over growth and inflation drove longer-dated yields higher yesterday and this is strongly negative for growth stocks.

UK local elections: Early results suggest bad news for the incumbent governing Conservative Party but perhaps not enough that would be a knockout blow for PM Johnson.

Cryptocurrency consolidates after big decline: A significant risk negative swing has seen a sharp sell-off across crypto. Bitcoin has fallen to its lowest since the Russian invasion of Ukraine, to around $36,500.

Economic Data:

- US Employment Situation (at 1330BST). The headline Nonfarm Payrolls are expected to reduce slightly to 391,000 in April (from 431,000 in March). Also, watch Average Hourly Earnings which are expected to drop slightly to 5.5% (from 5.6% in March). Unemployment is forecast to drop again to 3.5% (from 3.6%).

- Canada unemployment (at 1330BST). Canada is expected to have added +55,000 jobs in April (+72,500 in March) with the unemployment rate expected to fall to 5.2% (from 5.3%).

Major markets outlook

Broad outlook: Market sentiment has turned sharply sour again. USD outperformance is once more the key theme in forex, also impacting precious metals. Indices are under selling pressure too.

Forex: USD is decisively outperforming again. The AUD, NZD and GBP are key underperformers.

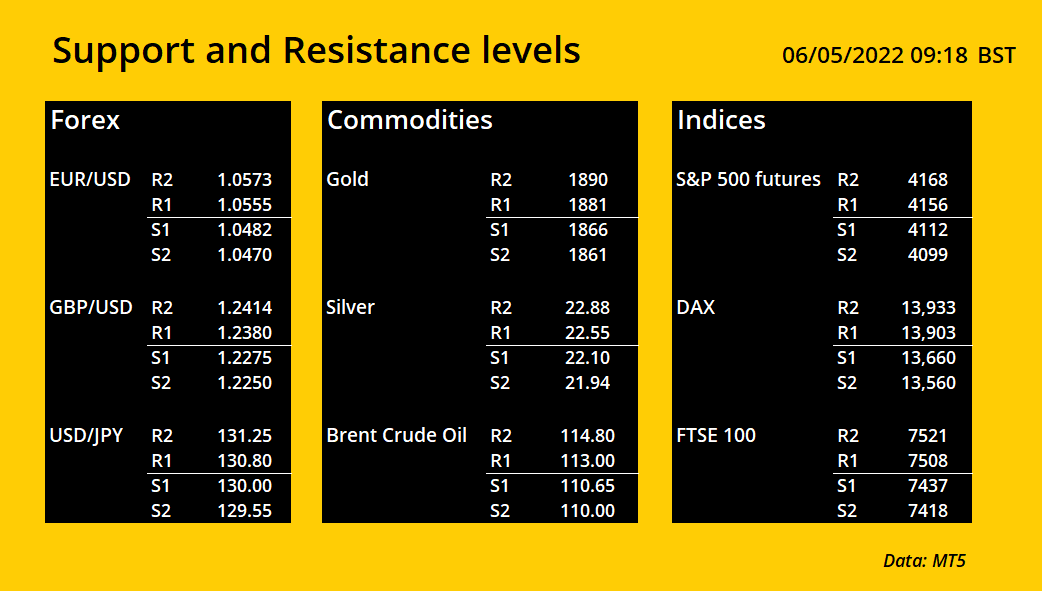

- EUR/USD recovery turned into sharp reverse yesterday and once more we see the support at 1.0470/1.0500 being pressured today. There seems to be no appetite to battle against USD strength right now. A break below 1.0470 opens 1.0325 (Dececmber 2016 key low) as the next support. Initial resistance is at 1.0550 with 1.0635 now key.

- GBP/USD a massive downside break of 1.2410 on the Bank of England yesterday has opened 1.2250 as the next support. Selling into strength continues to be the most viable strategy. Initial resistance is at 1.2380 this morning, but 1.2410/1.2475 is now a basis of overhead supply through the last week.

- AUD/USD posted a huge bear failure yesterday (it was not alone there) and the market has sold back sharply lower. With further weakness early today the potential for testing the key support at 0.7020 is once more likely. Initial resistance at 0.7130.

Commodities: Precious metals have fallen sharply again on USD strength. Oil has rallied towards range resistance.

- Gold has posted another bull failure around the $1910/$1920 resistance (adding to the importance of this resistance) and moved into retreat once more. The decline is back into important support around $1861/$1871 and how the market comes out of Nonfarm Payrolls could be key. Below $1850 opens $1820/$1825.

- Silver has fallen sharply back to a test of the key support around $22.00/$22.10 once more. With the decline early today, the downside pressure is mounting ahead of the US jobs report. Below $22.00 opens $21.40. Resistance is building overhead once more at around $22.50.

- Brent Crude oil has edged higher and is now within touching distance of a test of the range resistance around $116. Momentum is tentatively more positive, but RSI needs to move into the 60s to suggest decisive momentum. Initial support is around $110.00/$110.80. Above $116 opens the low $120s.

Indices: A massive bull failure on Wall Street has markets testing crucial support again. European markets have been weighed down by this move too.

- S&P 500 futures have retreated sharply from the key near to medium term resistance at 4303 and are testing the important support band 4100/4140. A close below this support would be a decisive downside break and open some considerable downside targets. Initial support would be 3950. A move above 4170 would help to stabilize the outlook slightly.

- DAX formed a “bearish engulfing” one day candlestick yesterday. The fact that this came at the resistance of the four-month downtrend increases the negative implications of this move. Selling into strength with lower highs and lower lows remains the strategy. A retest of 13,540 is now on. Initial resistance is 13,930/13,965.

- FTSE 100 has turned lower from 7462 and is now testing the initial support at 7438. With near term momentum turning corrective, a decisive breach of 7438 opens a move back towards the key reaction low at 7299. Initial resistance is at 7520.

This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. INFINOX is not authorised to provide investment advice. No opinion given in the material constitutes a recommendation by INFINOX or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.