Introduction

There is a raft of tier one data stateside that traders will be looking at this week. On top of that, Fed chair Powell’s semi-annual testimony to Congress will also take the eye. On a busy week, there are also two major central banks and UK inflation for traders to get stuck into.

- The Fed’s reaction to the inflationary pressure will be in focus this week, not only with US CPI but also the comments of Fed chair Powell on Wednesday.

- The Bank of Canada and Reserve Bank of New Zealand could give more hawkish hints this week.

- UK inflation will also be monitored as the Bank of England and the Fed jostle for position on who will tighten policy first.

It is all about the impact of inflation in the US this week

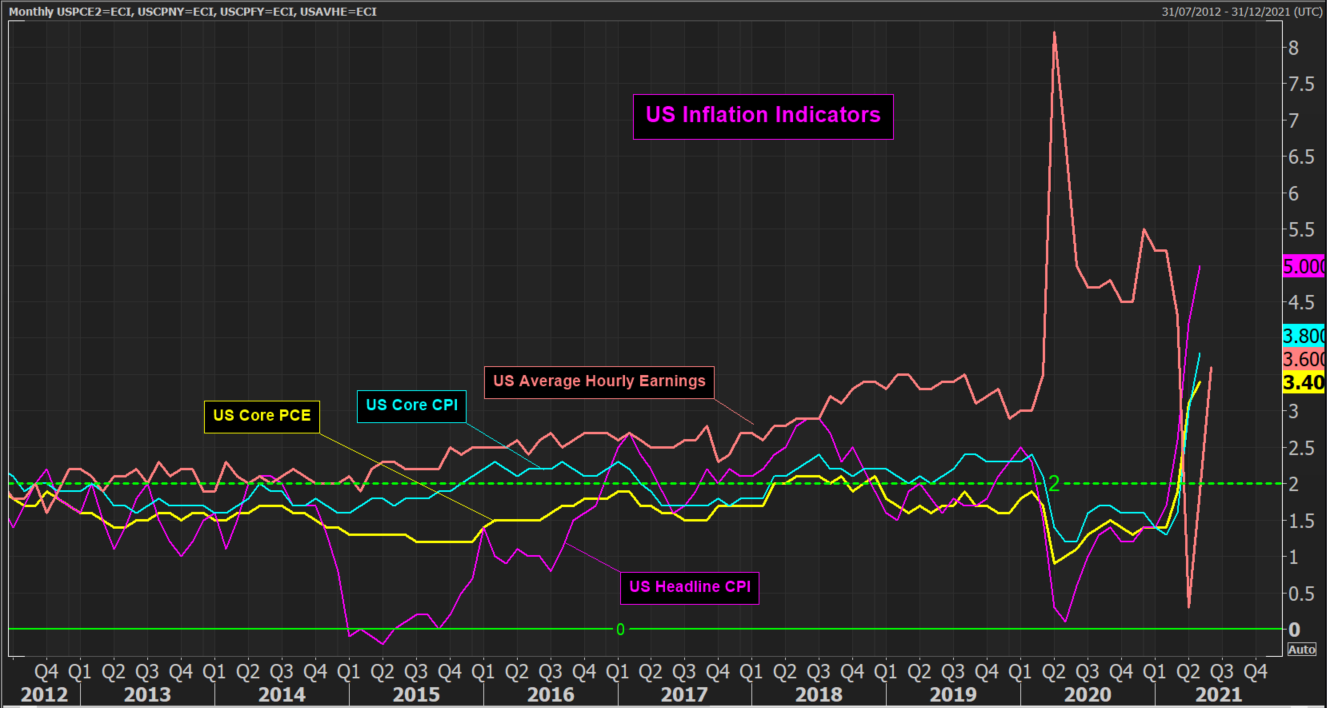

Tuesday sees US CPI inflation being top of the agenda on the calendar. With core CPI expected to rise to 4% (which would be the highest since 1992), the inevitable chat will be what impact this will have on the Federal Reserve. Survey data and sharp rises in input prices suggest that supply chain bottlenecks driving a shortage of labor (meaning higher wages) and high raw materials costs are feeding through to prices. The concern is that this will not be merely transitory.

The question for Fed Chair Powell at his semi-annual Congressional testimony on Wednesday will be how quickly the Fed sees inflation moderating. The natural step that markets will take from this is what it all means for the tapering of asset purchases perhaps later this year. Powell’s speech could be the key risk event of the week.

We also see Industrial Production (Thu) and Retail Sales (Fri) will also be watched. How much is industrial production being negatively impacted by the supply chain issues. For retail sales, there is an expectation for a second consecutive monthly decline in headline sales.

Market Impact: Watching for USD to be active all week, with impacts too across the risk spectrum

Bank of Canada to push on with its taper

The Bank of Canada is still the first real mover on tightening monetary policy. A successful rollout of the COVID vaccination (one of the best in the world) and continued improvement in labour market statistics has enabled the BoC to begin to normalise monetary policy sooner than any other major central bank.

It has already begun to taper its asset purchases (down from C$5bn per week to C$3bn per week). This could be stepped up with a further reduction perhaps down to C$2bn per week).

Market impact: CAD has suffered amidst a risk reduction and USD bounce, however, we still see CAD as well-positioned for outperformance.

The Reserve Bank of New Zealand is another bank on the tightening path, since signalling in May that its projected path for the OCR (the interest rate) suggested a rate hike in late 2022. The initial step towards this is to taper asset purchases. The concerns surrounding the Delta variant of COVID may make it too soon during this meeting though.

Market impact: NZD will likely continue to outperform AUD in the coming months

UK inflation to tick higher

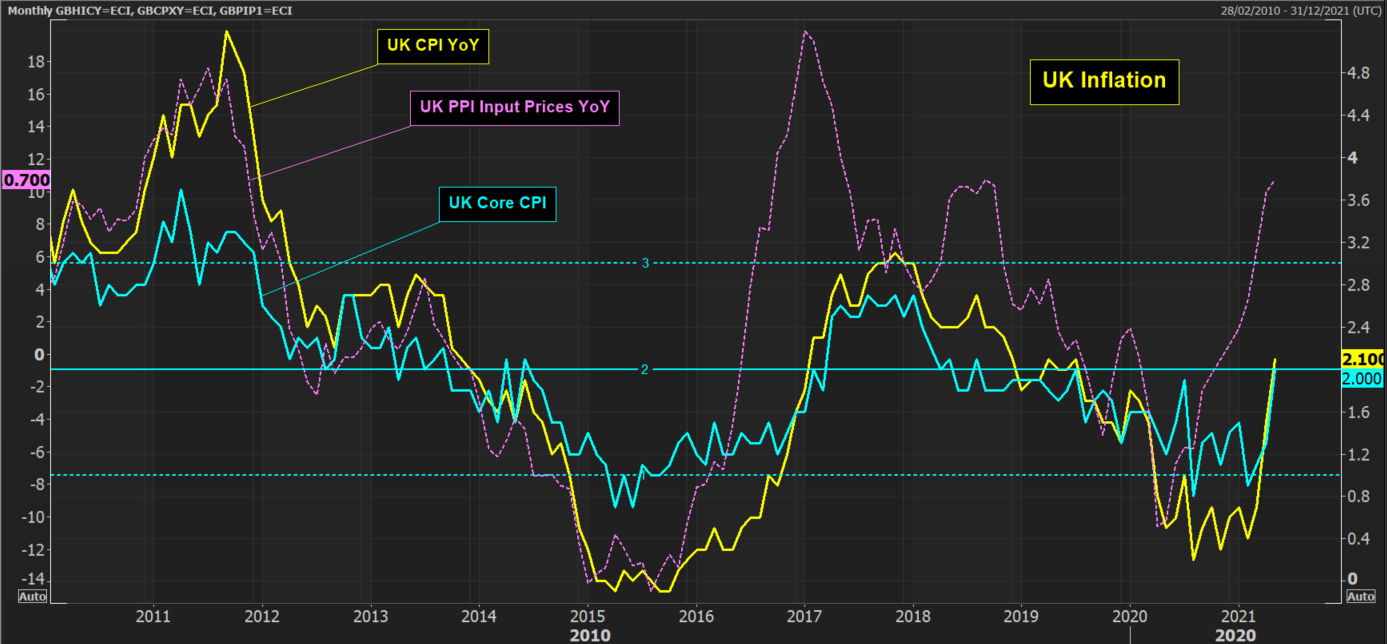

Core UK inflation jumped sharply in May as both core and headline CPI increased to +2.0% and +2.1% respectively. The input price rises are a key factor of this (as they are for many major economies). Further input price rises will likely be pushed onto the consumer and show up in the CPI data in the coming months.

Consensus is expecting a fairly stable +2% for core and +2.2% for headline inflation. We caution against reading too much into data surprises here with such a volatile few months ahead expected for inflation.

Market reaction: GBP to move but may struggle for sustained traction unless a significant surprise is seen.

Conclusion

US data and Fed chair Powell will be key this week. However, there are also two major central banks that traders will be looking for hawkish hints from. UK inflation is also on the docket.