After the volatility of recent days, the economic calendar is looking rather more sedate this week. Inflation remains a crucial conundrum for central banks of the major economies of the world. US CPI will subsequently take the key focus for traders this week, in addition to inflation indications taken from the PPI and Michigan Sentiment. Inflation indicators from China and Australia are also on the calendar. Elsewhere, the first look at UK Q1 GDP will be of interest after the Bank of England’s gloomy assessment of the UK economy last week. In Latin America, we are on the lookout for Mexican and Brazilian inflation and the Mexican central bank’s rate decision.

Watch for:

- North America – US CPI, PPI and prelim Michigan Sentiment

- Europe & Asia – German ZEW, China CPI and UK Q1 GDP

- Latin America – Mexican and inflation and central bank interest rates, Brazilian inflation

North American data:

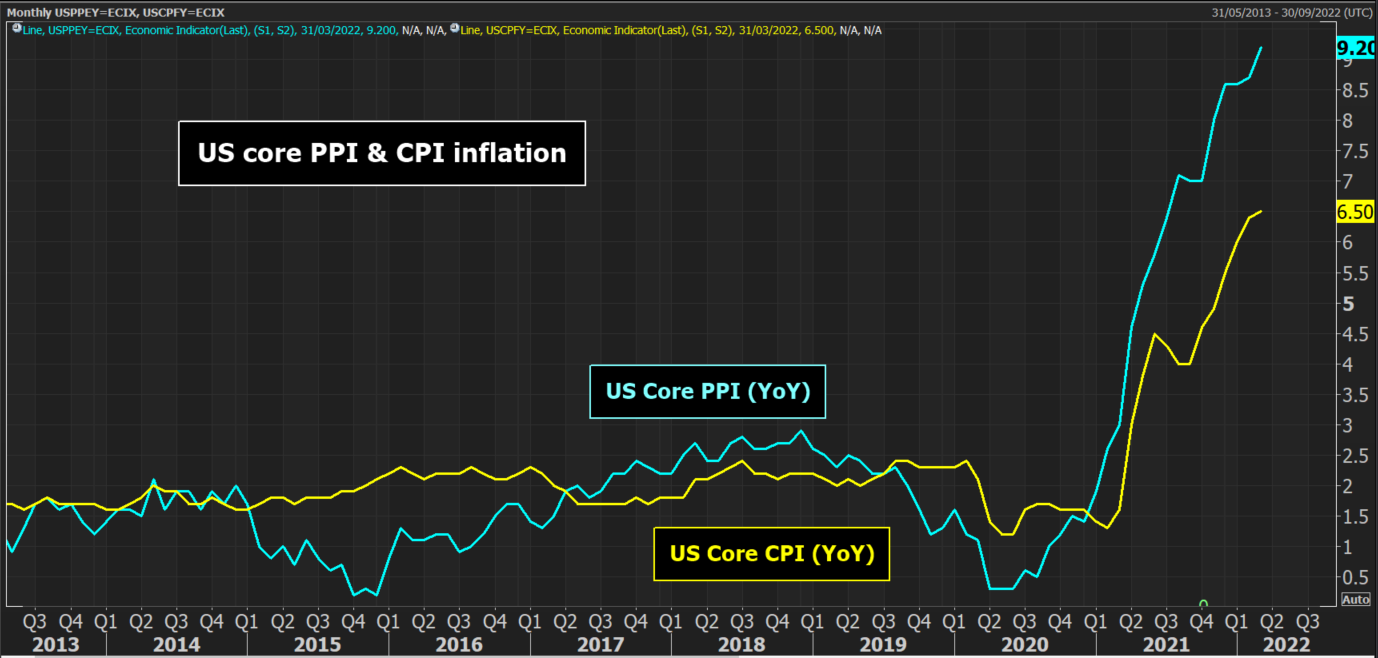

- US CPI (Wednesday 11th May, 1330BST) Headline CPI is expected to increase to 8.8% in April (from 8.5% in March). The core CPI is expected to increase slightly to 6.6% (from 6.5%).

- US PPI (Thursday 12th May, 1330BST) Headline PPI inflation is expected to increase to 11.6% in April (from 11.2% in March), with core PPI increasing to 9.3% (from 9.2%)

- US Weekly Jobless Claims (Thursday 12th May, 1330BST) Weekly claims are expected to increase marginally to 205,000 (from 200,000 last week)

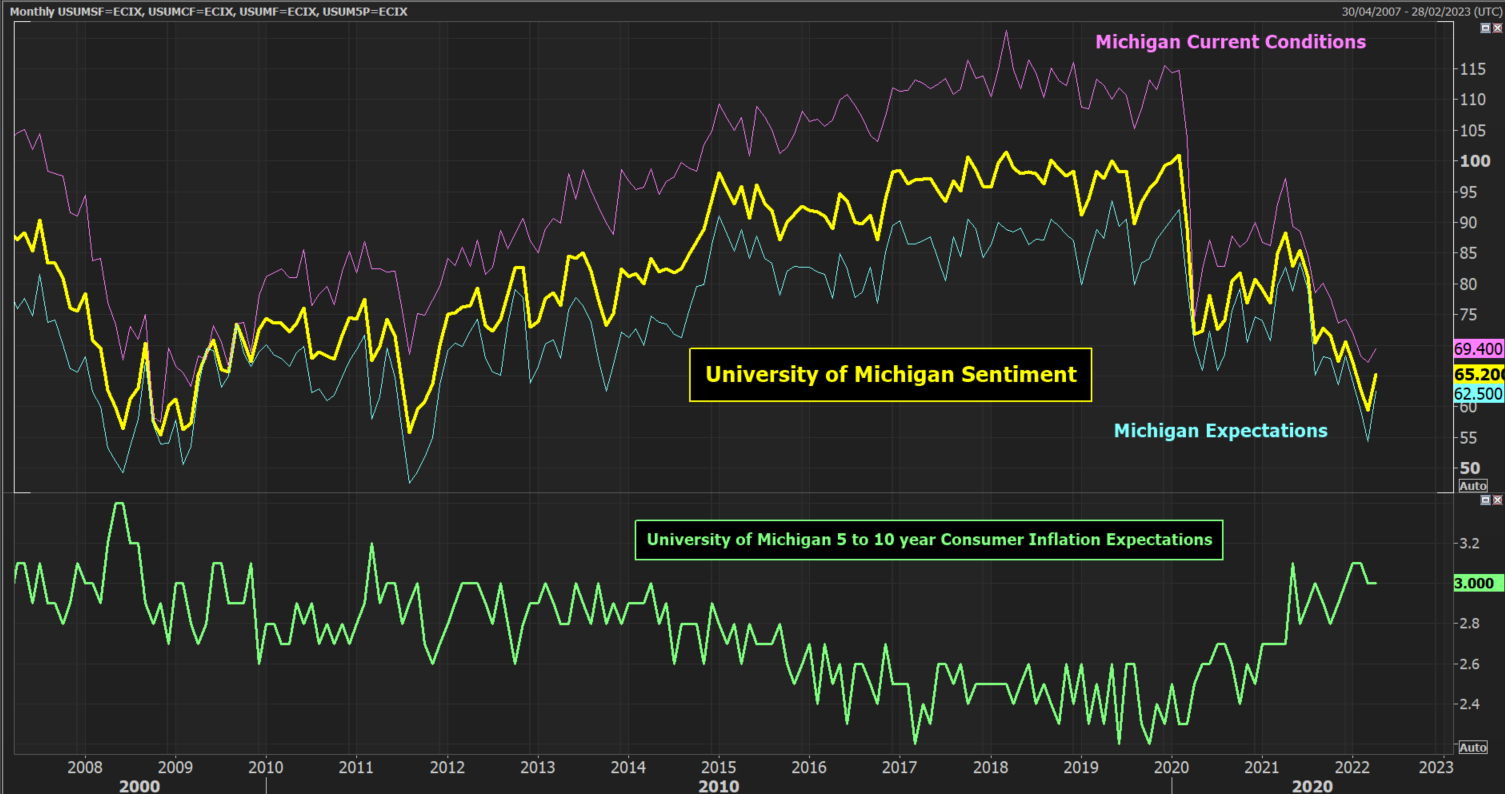

- Michigan Sentiment – prelim (Friday 13th May, 1330BST) Sentiment is expected to deteriorate to 63.8 in May (down from a final 65.2 in April).

There are limited US data points this week, but there are a couple of key ones. US inflation trends continue to run higher, but there were signs in the core CPI last month that peak inflation may be approaching. The assessment of how this is reflected in the April data will be key for US CPI and US PPI. Both are expected to increase only marginally.

Michigan Sentiment is expected to deteriorate in April, driven by declines in both current conditions and expectations. This would reverse the improvement that was seen in March data. However, the focus will also be on the consumer inflation expectations which remain around 8-year highs, but have shown signs of stabilizing recently.

Market Reaction:

- US yields and USD will see elevated volatility around CPI and PPI surprises.

- Michigan Sentiment will also be watched for renewed deterioration, with a risk negative bias likely

Europe & Asia:

- German ZEW Economic Sentiment (Tuesday 10th May, 1000BST) Sentiment is expected to remain steady at -40.5 in May (-41.0 in April)

- China CPI (Wednesday 11th May, 0230BST) CPI inflation is expected to increase slightly to 1.6% in April (up from 1.5% in March). The PPI is expected to slip slightly to 7.8% (from 8.3%)

- Australian inflation expectations (Thursday 12th May, 0200BST) Expectations of inflation are expected to reduce slightly to 4.8% in May (from 5.2% in April)

- UK GDP – prelim (Thursday 12th May, 0700BST) Q1 GDP is expected to come in at 0.9% (after a final +1.3% in Q4)

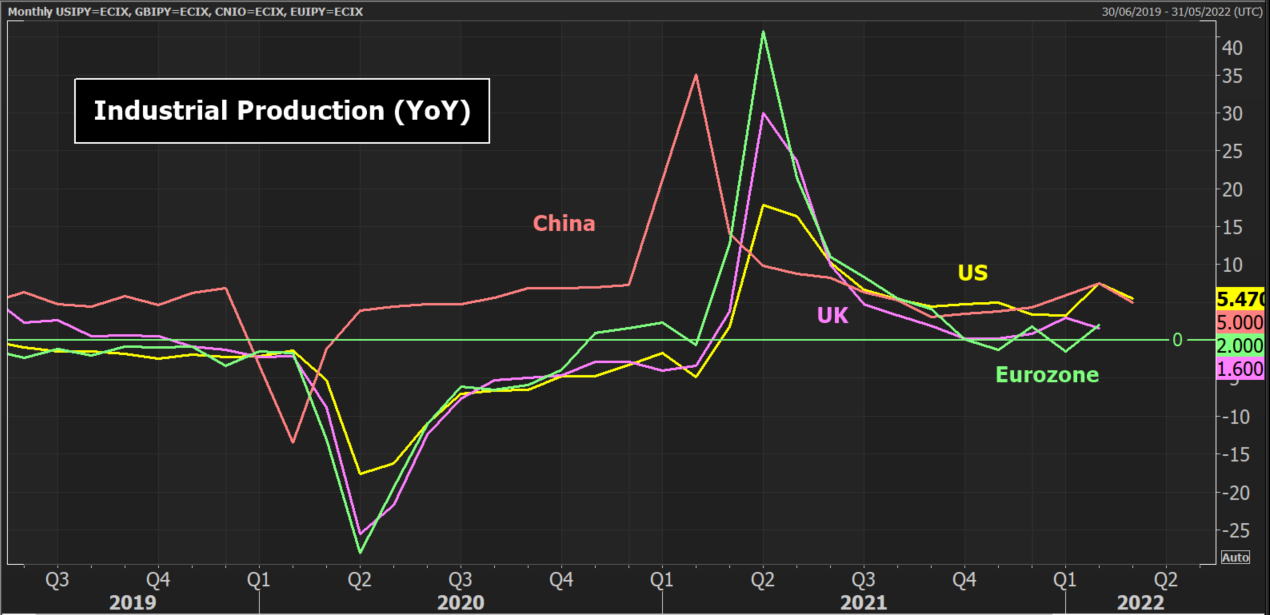

- UK Industrial Production (Thursday 12th May, 0700BST) With just +0.1% industrial production forecast, the year on year production is expected to drop back to +1.0% in March (from +1.6% in February)

- Eurozone Industrial Production (Friday 13th May, 1000BST) Monthly production is expected to fall by -1.0% in March

Inflation will also be watched in China this week. A tick higher is expected for the CPI, but the consensus is expecting a slight decline in the PPI. Factory gate inflation moderating to 7.8%, reflecting the COVID lockdown, but also could this be another signal for inflation trends beginning to peak?

The first reading of UK Q1 GDP is expected to be at 0.9%. This is also the Bank of England’s expectation, so any undershoot would be a concern, especially for GBP. We are also looking for UK Industrial Production trends too which are declining in the major economies. March looks to have been a subdued month for the UK, with consensus forecasting 12-month production to fall to around 1%. Deterioration is also expected in the Eurozone Industrial Production, where a monthly decline could see production close to flat on a 12-month basis.

Market Reaction:

- A negative surprise in the German ZEW would be negative for EUR

- Negative surprises for Chinese inflation may impact risk appetite

- GBP traders will watch for any surprises in the UK growth data

Latin America:

- Mexico inflation (Monday 9th May, 1200BST) Year on year inflation is expected to increase to 7.78% in April (up from 7.45 in March). Core inflation is expected to increase more moderately to 6.81% (from 6.78%)

- Brazil Retail Sales (Tuesday 10th May, 1300BST) Sales are expected to decline by -0.3% in March which would leave 12-month sales at -1.1% (from +1.3% in February)

- Brazil inflation (Wednesday 11th May, 1200BST) Year on year inflation is expected to increase sharply to +12.32% in April (from +11.30% in March)

- Mexico Industrial Production (Thursday 12th May, 1200BST) Production is expected to deteriorate to -3.2% in March (down from 2.5% in February)

- Mexican central bank interest rates (Thursday 12th May, 1900BST) Expectation is for a +50bps hike to 7.00% (form 6.50%)

- Colombia Retail Sales (Friday 13th May, 1600BST) 12-month sales are expected to decline to 2.5% in March (from 4.9% in February).

- Colombia Industrial Production (Friday 13th May, 1600BST) 12-month production is expected to deteriorate to +4.6% in March (from 10.7% in February).

Inflation will be a hot topic for Lat Am this week, with both Mexico and Brazil data due. After stalling around the turn of the year, inflation has taken off once more. Headline Mexican inflation is expected to continue higher, although the core data is expected to be all but steady. This may play into the mindset of the Mexican central bank which is expected to increase rates by 0.5% and move the rate above core inflation.

In Brazil, the central bank hiked rates by another 100 basis points last week (the 10th rate hike in a row) in an attempt to stay ahead of the inflation rise which “continued to surprise negatively”. However, with Brazil inflation set to increase by another +1% this week, further rate hikes are likely, even if they will be “of smaller magnitude” at the next meeting in mid-June.

Market Reaction

- Expect elevated volatility on MXN and BRL this week as inflation (and subsequently interest rates) are the key factor.

This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. INFINOX is not authorised to provide investment advice. No opinion given in the material constitutes a recommendation by INFINOX or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.